How to Choose the Right Business Structure

For first-time entrepreneurs, starting a business is exciting and a little bit daunting. There are three main types of business structure for small businesses to consider based on the size, complexity and needs of your business. Here’s a quick guide to get you started when choosing a structure for your new business idea.

How to Choose the Right Legal Structure for Your Business

Before determining the right structure for starting your own business, you need to consider a few important questions. Are you planning to work alone or hire employees? Will you seek outside funding? Do you need personal liability protection? Are you looking for tax advantages or a simple structure? Get out a piece of paper and write out everything that comes to mind—including your hopes, dreams and ideas for this business. Starting here will provide more clarity before you choose a structure.

Types of Structure for Small Businesses

There are three main structures to choose from when starting a business.

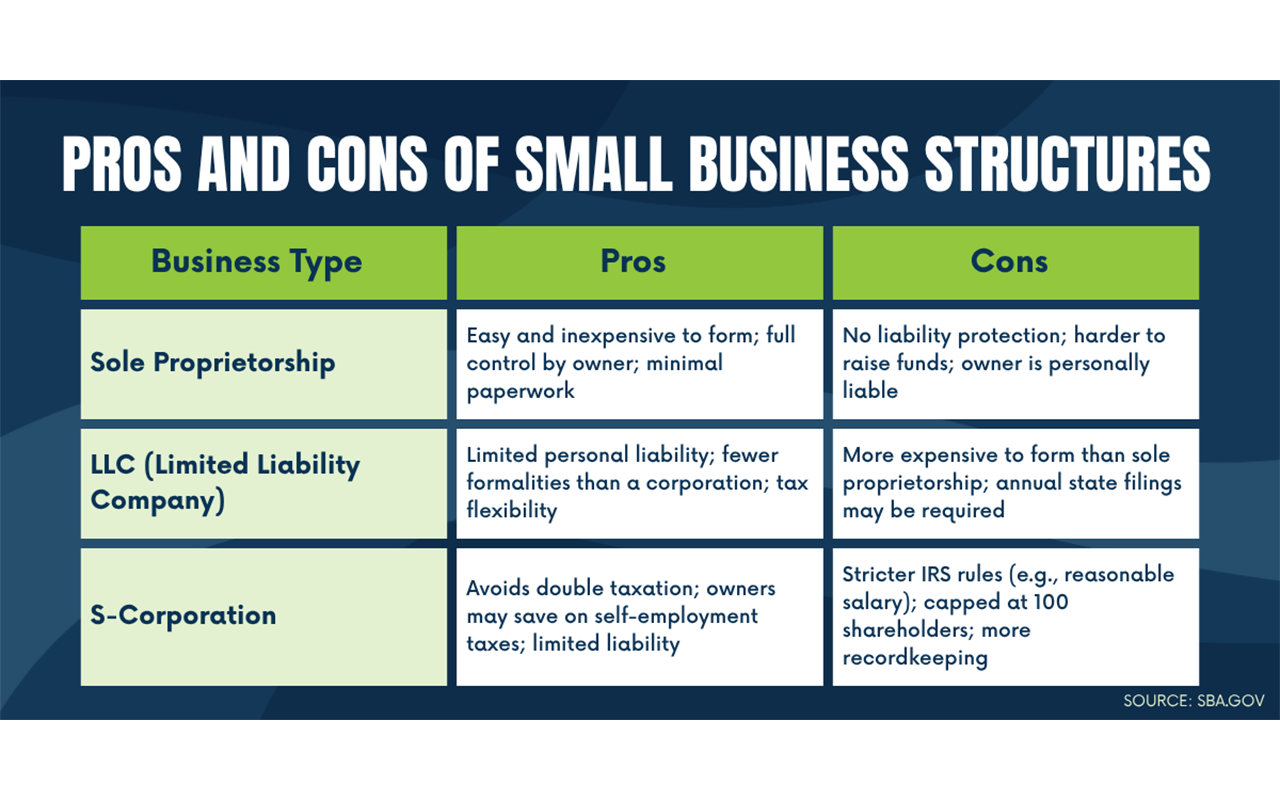

Sole Proprietorship

In a sole proprietorship, you do not create a separate business entity—which means that your business assets and liabilities are not separated from your personal ones. According to the U.S. Small Business Administration, this is the easiest and least expensive structure to set up, and gives you more control over your business. You are automatically considered a sole proprietorship if you do not register your business as any other type but begin doing business.

Day-to-Day: Sole Proprietorship

| Taxes | Income taxed on owner's return (Schedule C) |

|---|---|

| Liability | Personal assets at risk |

| Operations | Simple |

Might be a good option for freelancers, consultants or entrepreneurs starting out with a low-cost setup.

Limited Liability Company (LLC)

A limited liability company is a hybrid structure that protects your personal assets as a corporation does but includes more flexible tax options. According to the IRS, your LLC can have one or more owners referred to as “members.” Some business types, such as banks and insurance companies, are not eligible to register as an LLC.

Day-to-Day: LLC

| Taxes | Can choose to be taxed as sole prop, partnership or corporation |

|---|---|

| Liability | Personal assets protected |

| Operations | Moderate complexity |

Might be a good option for small business owners looking for personal liability protection without losing flexibility and tax options.

S Corporation (S-Corp)

An S Corporation is a special tax status that allows profits and losses to pass through to the owner’s personal tax return. According to the IRS, this special tax status can help business owners avoid double taxation. You must meet a certain list of requirements (including having no more than 100 shareholders) to be eligible to register as an S corporation.

Day-to-Day: S-Corp

| Taxes | Pass-through + potential self-employment tax savings |

|---|---|

| Liability | Personal assets protected |

| Operations | Requires salary / payroll, shareholder limits |

Might be a good option for business owners whose business is growing and are ready to meet stricter IRS requirements while saving on self-employment taxes.

What’s a DBA?

When running a business, you might operate day-to-day under a different name than your registered legal name. For instance, a smoothie shop could register as Tiki Incorporated LLC and then promote itself under the name Tiki Hut Smoothies. This is referred to as a DBA (doing business as) and can also be called a trade name, fictitious business name or assumed name.

This might be done for branding purposes, to make your business more marketable or when someone is running multiple businesses under one registered entity.

Pros and Cons of Each Business Structure

If your business is still in the early stages and you’re not sure how you want to structure it, here are some of the pros and cons to consider for each registration type.

Can I Change My Business Structure Later?

If you’re not feeling confident in your choice of business structure—fear not. You can still change it later. According to the IRS, you can start as a sole proprietor and then later form an LLC or elect S-corporation status. Whether you change your mind or your business needs simply evolve, your structure can evolve too. Be sure to talk to a certified financial planner for help in changing your tax classification.

Registering Your Small Business in Florida

Ready to get things moving? This helpful checklist can help you gather everything you need once you are ready to register your small business in Florida.

Consulting an Expert

While you are the one who holds all the hopes and dreams for your new business, it’s always a good idea to outsource some of the more technical considerations to an expert who can guide you in the right direction. A certified financial planner (or CPA) can help you avoid common startup mistakes and compare tax impacts of different structures when starting your small business.

At Harvard & Associates, CPA, we provide expert accounting solutions tailored to your needs, helping you save time, reduce stress and maximize your financial potential. Our team of CPAs is experienced, knowledgeable and dedicated to providing financial guidance, strategic tax planning and reliable accounting solutions.

With offices in Tallahassee, Florida and Thomasville, Georgia, Harvard & Associates can provide you with the bookkeeping, tax and financial services you need. Whether you're an individual, a small business or a growing enterprise, we're here to help. Call us at (850) 224-9008 or contact us online to start a long-term relationship with the local accounting expertise and service you expect.

DISCLAIMER: This blog is for informational purposes only and does not constitute legal, financial or tax advice. Consult a licensed tax professional or accountant at Harvard and Associates for advice specific to your situation.